I want to talk about one of the most dangerous ideas in retirement planning.

Not dangerous because it’s wrong, exactly. Dangerous because it’s right enough to feel safe — and wrong enough to quietly wreck a plan.

The 4% rule. Thirty years old, universally taught, and still the first answer most people get when they ask how much they can spend in retirement. Pull out 4% of your portfolio in year one, adjust for inflation every year after that, and you’ll be fine for 30 years.

That was the finding of financial advisor Bill Bengen in 1994. His research was solid. His math was real. His data stretched back to 1926. And in the world of the mid-1990s — decent bond yields, reasonable valuations, tame inflation — 4% was a defensible number.

That world is gone.

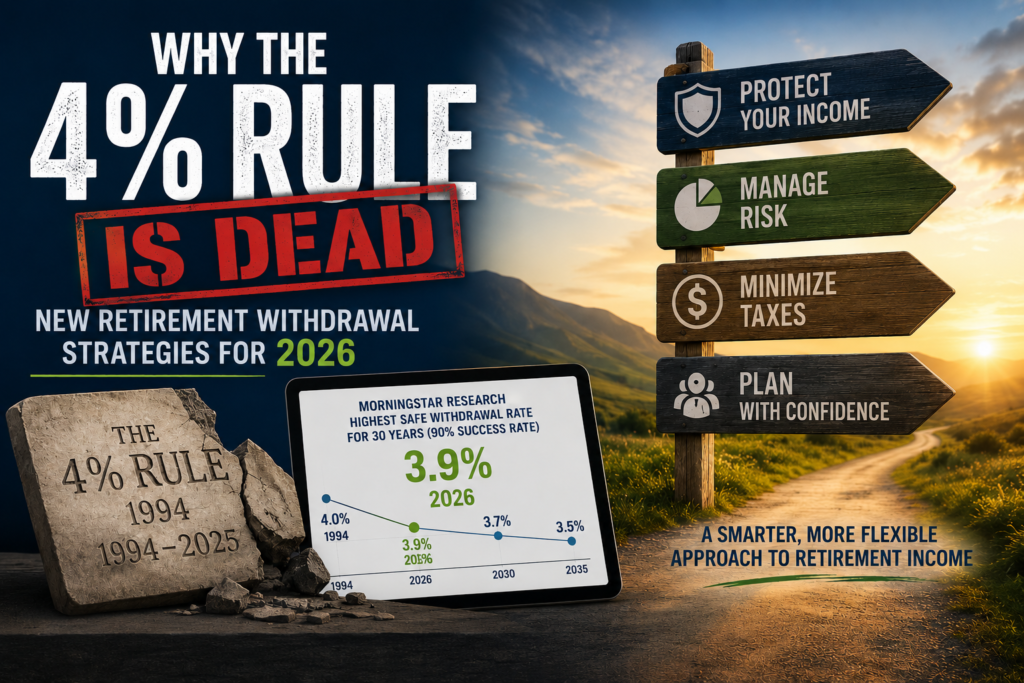

What the Research Actually Says in 2026

Morningstar publishes an annual deep-dive on retirement withdrawal rates, and their December 2025

State of Retirement Income report is the most current data we have. Their conclusion for someone

retiring in 2026: the highest safe starting withdrawal rate for a balanced portfolio over a 30-year horizon

— with a 90% probability of not running out of money — is 3.9%.

Not 4%. Not 5%. Three-point-nine percent.

On a $1 million portfolio, the difference between 4% and 3.9% is $1,000 a year. That’s not the point.

The point is what’s underneath the number: Morningstar builds their models using forward-looking

return assumptions, not historical averages. They’re looking at where bond yields are headed, what

equity valuations suggest about future returns, and what inflation is projected to do. That methodology

is more honest than assuming the next 30 years will look like the last 100.

The 4% rule was built for a world of 6% bond yields. We don’t live there anymore. Plugging 1994 data

into a 2026 retirement is like using a 1994 map to navigate a city that’s been completely rebuilt.

The Real Villain: Sequence of Returns Risk

Here’s the thing that gets almost no attention in the 4% rule conversation: when bad markets happen

matters as much as whether they happen at all.

If you retire in a good market and your portfolio grows for the first five years, you may have a better position to handle a bear market later. But if a serious downturn hits in year one or two — right when

you’re taking withdrawals and the portfolio is at its largest — the math breaks in ways that are very hard to recover from. You’re selling into a down market to fund your lifestyle. Every dollar pulled out at depressed prices is a dollar that can’t participate in the eventual recovery.

I watched this play out in real time in 2022. Clients who had been told “just follow the 4% rule” were

suddenly withdrawing a larger and larger percentage of a rapidly shrinking portfolio. That’s not a plan.

That’s a calculation that forgot to account for the real world.

Morningstar’s research confirmed what I’ve seen in my practice: retirees who experienced poor returns

in the first five years and didn’t adjust their spending were far more likely to exhaust their portfolios

before the end of a 30-year horizon.

What Actually Works: Four Strategies for 2026

A Custom Financial Plan Built Around Your Numbers. The most important thing I can tell you is

that no withdrawal rate — 4%, 3.9%, or anything else — means anything in isolation. The number only

makes sense in the context of a full picture: your income sources, your tax situation, your health, your

actual spending, and how all of those interact over time. At Creative Financial Group, we don’t hand

clients a percentage and wish them luck. We build a personalized withdrawal plan that accounts for

every income stream — Social Security timing, RMDs, taxable accounts, Roth accounts — and

sequences them in the order that minimizes taxes and maximizes longevity. That’s what a plan is. A

rate of return assumption is a math problem. A plan is a strategy.

The CFG Bucket Strategy. Rather than applying a single withdrawal rate to the whole portfolio, we

organize assets into two or three buckets based on when you’ll need the money. Near-term income

needs are funded from safe, liquid assets that never depend on what the market is doing that week.

Longer-term assets stay invested for growth. The bucket structure solves the sequence of returns

problem at its root — you’re never forced to sell at the wrong time because the money you need in the

short run is already set aside.

Risk Management Layered Into Every Decision. Withdrawal strategy and risk management aren’t

separate conversations. They’re the same conversation. For clients with significant assets in fixed

indexed annuities, we use those guaranteed income floors to define a baseline that the portfolio never

has to carry alone. That guaranteed income layer is subject to the claims paying ability of the insurer

and protects the downside while still participating in upside — changing how confidently a client can

spend from their investment portfolio. We also build explicit stress tests into every plan: what happens if

markets drop 30% in year two? What happens if one spouse lives to 95? What if healthcare costs spike

in the last decade? A plan that hasn’t been tested against those scenarios isn’t a plan — it’s a

projection dressed up as one.

A Plan That Gets Updated, Not Forgotten. This is where the 4% rule fails most quietly — it treats

retirement as a static event rather than a 30-year journey. Life doesn’t hold still. Markets move. Tax

laws change. A spouse passes. A health diagnosis arrives. A child needs help. At CFG, every client’s

plan is monitored on an ongoing basis and adjusted when something significant changes — not just at

annual review time, but whenever life calls for it. The withdrawal strategy that made sense at 65 may

need to look different at 72. That’s not a failure of the plan. That’s the plan working exactly the way it

should.

The Retirement Spending Smile

One more thing the 4% rule gets wrong: it assumes your spending stays constant forever.

Research by economist David Blanchett — often called the “retirement spending smile” — shows that

real retiree spending tends to fall in the slow-go years (roughly ages 75–85) and then rise again late in

life when healthcare costs spike. The traditional 4% rule adjusts withdrawals upward for inflation every

single year, building in a spending pattern that doesn’t match how most people actually live.

Morningstar’s own modeling found that simply acknowledging this natural spending pattern can effectively raise a safe starting withdrawal rate by about 1 percentage point — without any additional

portfolio risk.

Clients who have carefully estimated their actual spending trajectory across retirement — not just

assumed a flat number forever — end up with far more flexibility and far less anxiety than clients

chasing a rule of thumb from 1994.

The Bottom Line

The 4% rule was a starting point, not an endpoint. It was a reasonable approximation for a different era,built on data that no longer reflects the return environment we’re planning through. For 2026, the

research says 3.9% is the conservative anchor — and a well-built plan done right can get you

meaningfully higher than that.

But the bigger shift isn’t the percentage. It’s the mindset. Retirement withdrawal isn’t a formula you set

once and walk away from. It’s a living plan that needs to respond to markets, to taxes, to how your

spending actually changes over time, and to the income sources you’ve built alongside your portfolio.

If you’re still working off the 4% rule, you’re not working off a plan. You’re working off a guess that’s

three decades old.

Want a personalized retirement withdrawal plan built around your exact numbers? Schedule a

retirement tax review with me at Creative Financial Group.

Kurt Supe is a CPA and co-founder of Creative Financial Group, a retirement planning firm based in Indiana. He

has spent nearly 30 years helping clients build and execute retirement income strategies that account for taxes,

markets, and the real cost of a life well-lived. Morningstar withdrawal rate data referenced from the State of

Retirement Income: 2025 Edition, published December 3, 2025.

This blog is for educational purposes and does not constitute personalized financial, tax, or investment advice.

Individual circumstances vary.